As artificial intelligence, electric vehicles, and advanced defense technologies reshape the global economy, nations are discovering that the most valuable strategic assets may no longer be oil fields or military bases, but the minerals buried beneath the earth.

For much of the twentieth century, geopolitics revolved around one commodity. Oil determined alliances, fueled wars, shaped foreign policy, and transformed deserts into economic powers. Whoever controlled energy often influenced global politics.

Today, another strategic resource is quietly taking its place.

The world’s major powers are no longer competing simply to secure access to energy. They are competing to secure the minerals that will determine who builds the next generation of economies. Lithium, cobalt, graphite, nickel, copper, and rare earth elements have become the foundation of electric vehicles, artificial intelligence, semiconductors, renewable energy systems, satellites, drones, and precision-guided weapons. The race to control these materials is rapidly becoming one of the defining geopolitical struggles of the twenty-first century.

This new competition is not driven by ideology in the traditional sense. It is driven by technology. Every breakthrough in artificial intelligence requires vast computing infrastructure. Every electric vehicle depends on battery minerals. Every advanced fighter aircraft, missile system, and communications satellite relies on specialized materials that only a handful of countries can supply.

The result is a geopolitical landscape where mines have become almost as strategically important as military bases.

The urgency surrounding critical minerals has grown because governments increasingly view them not merely as economic assets but as national security necessities. Modern militaries cannot function without them. Clean energy transitions cannot accelerate without them. Digital economies cannot expand without reliable access to these resources. In an era where technological superiority increasingly defines global influence, the supply of critical minerals has become inseparable from national power.

No country illustrates this reality more clearly than China.

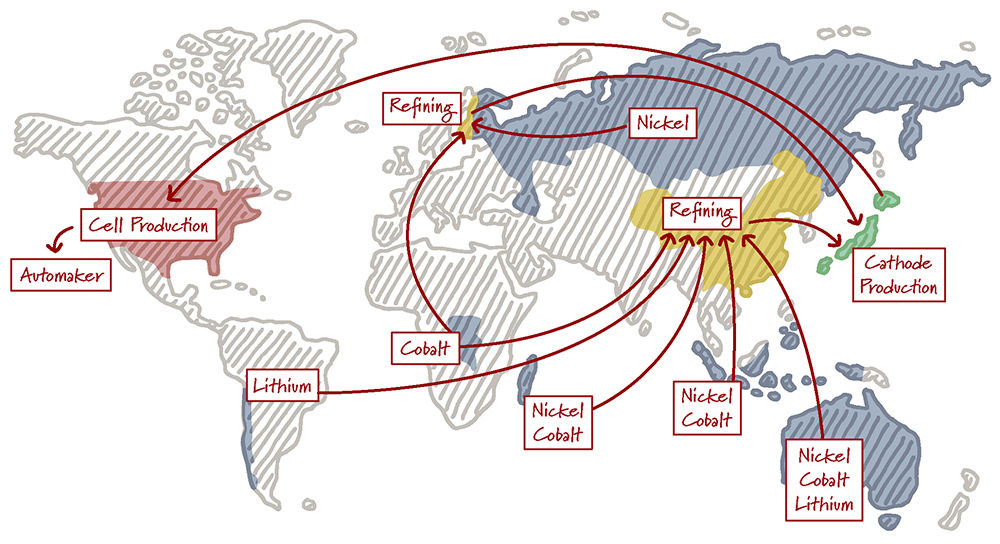

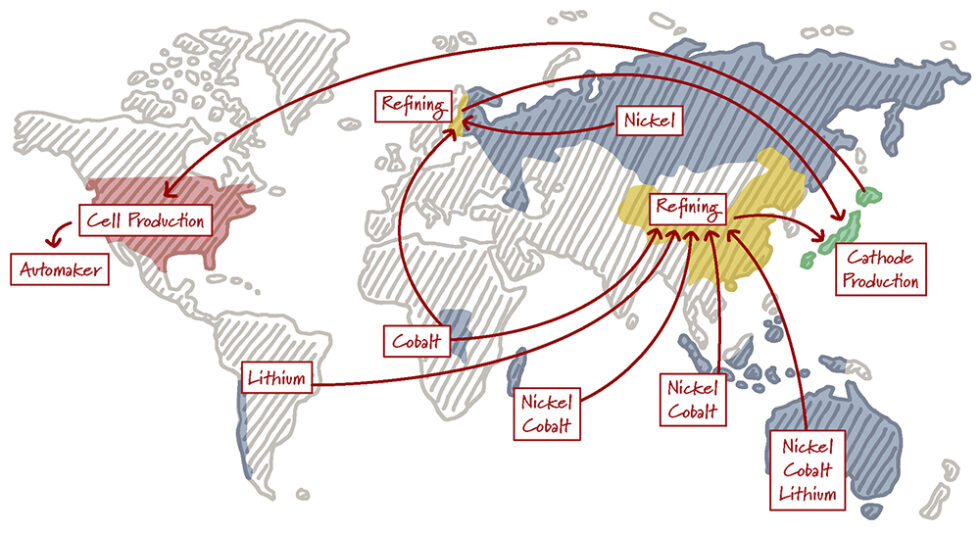

Although China does not possess every major mineral reserve, it has spent decades building something arguably more valuable: dominance over processing, refining, and manufacturing. Mining represents only the first step in the supply chain. Raw minerals must be refined into highly specialized materials before they can be used in batteries, magnets, electronics, and defense systems. It is in this stage that China has built an extraordinary advantage.

Over many years, Beijing invested heavily in refining capacity, chemical processing, infrastructure, industrial policy, and downstream manufacturing. Today, much of the world’s rare earth processing takes place inside China, alongside significant portions of global graphite processing and battery component production. This means that even minerals extracted from Africa, Australia, or Latin America often travel to Chinese facilities before reaching global manufacturers.

That concentration has transformed an economic advantage into strategic leverage.

Recent export restrictions on certain rare earth products and processing technologies have reminded governments that supply chains can become geopolitical tools. Just as oil embargoes once altered international politics, disruptions in mineral processing now carry the potential to slow automobile production, delay renewable energy projects, constrain semiconductor manufacturing, and complicate defense procurement.

The lesson has been unmistakable.

Dependence on a single supplier for materials that underpin modern economies creates vulnerabilities that governments can no longer ignore.

That realization has reshaped policy across much of the developed world. The United States, the European Union, Japan, Canada, Australia, and other partners are now investing billions of dollars to diversify critical mineral supply chains. Rather than relying overwhelmingly on one country, they are pursuing a strategy built around trusted partners, domestic production, recycling, and new refining capacity.

The G7 has increasingly framed critical minerals not simply as a commercial issue but as an essential pillar of economic resilience. Governments are supporting new mines, financing processing facilities, encouraging private investment, and negotiating partnerships with resource-rich countries. The objective is not necessarily to replace China overnight—a task that would be extraordinarily difficult—but to reduce strategic dependence over time.

This effort is transforming investment patterns across the globe.

Countries once viewed primarily as commodity exporters are becoming central actors in international strategy. Australia is expanding production of lithium and rare earths. Canada is positioning itself as a reliable supplier for North American industries. Greenland’s untapped mineral deposits have attracted growing international attention despite their harsh geography. Across Latin America, lithium-rich regions have become increasingly significant for global battery production.

Yet nowhere is the geopolitical importance of critical minerals more evident than in Africa.

The continent possesses some of the world’s largest reserves of cobalt, graphite, manganese, platinum, and numerous other strategic resources essential to modern industry. What was once seen primarily as a source of raw commodities is increasingly viewed as a cornerstone of the global energy transition and technological revolution.

As demand rises, governments and corporations from around the world are competing to secure long-term mining rights, infrastructure agreements, processing investments, and political partnerships across the continent.

This competition presents both opportunity and risk.

For African governments, critical minerals offer the possibility of industrial development, infrastructure investment, employment, and greater geopolitical influence. But history also offers cautionary lessons. Resource wealth has too often generated dependency rather than development when value-added manufacturing occurred elsewhere.

Many African leaders are therefore seeking not only mining investment but also local processing, technology transfer, and manufacturing capacity. The debate is no longer simply about exporting minerals; it is about capturing a greater share of the industries those minerals enable.

Technology itself is accelerating this race.

Artificial intelligence has dramatically increased demand for advanced data centers, semiconductor manufacturing, and sophisticated computing hardware. Renewable energy systems require enormous quantities of copper for electrical transmission and rare earth magnets for wind turbines. Electric vehicles depend on battery minerals whose demand is expected to remain strong as transportation continues to electrify. Modern defense systems—from guided missiles and naval propulsion systems to radar, drones, and secure communications—depend upon highly specialized materials that cannot easily be substituted.

Every major technological trend points toward greater mineral intensity rather than less.

This convergence of digital transformation, clean energy, and military modernization explains why governments increasingly speak about mineral security with the same urgency once reserved for oil security.

Unlike previous eras, however, the contest is not solely about controlling natural deposits. It is equally about controlling refining technology, manufacturing ecosystems, logistics networks, environmental standards, financing, and intellectual property. The countries that dominate these stages capture far greater economic value than those that merely extract raw materials.

In many respects, the emerging competition is more complex than the twentieth-century struggle over oil.

Oil could be transported, stored, and traded through relatively straightforward global markets. Critical mineral supply chains involve multiple stages spread across different continents, each vulnerable to geopolitical disruption. A disruption in refining capacity, shipping, environmental regulation, or processing technology can ripple through industries thousands of miles away.

That complexity is already reshaping international diplomacy.

Trade agreements increasingly include provisions on mineral cooperation. Security partnerships now extend beyond military exercises to include resource development. Development finance institutions are supporting mining projects once considered purely commercial ventures. Economic policy and national security are becoming increasingly intertwined.

The result is a world in which geology is once again influencing geopolitics—but in an entirely new way.

The Cold War of the twentieth century revolved around ideology and nuclear deterrence. The strategic competition of the twenty-first century revolves around technological leadership and industrial resilience. Whoever controls the materials that power advanced technologies may ultimately shape global economic leadership itself.

The minerals buried beneath remote deserts, mountain ranges, and forests are no longer just geological assets. They have become strategic foundations for the industries that will define the coming decades.

So, will the countries that control critical minerals enjoy the same strategic advantage that oil-producing nations held during the twentieth century?

Not exactly—but perhaps something even more consequential.

Oil powered economies. Critical minerals power the technologies that will determine economic competitiveness, military capability, digital innovation, and geopolitical influence simultaneously. In the decades ahead, the greatest source of global power may not belong to the countries with the largest armies or even the largest energy reserves, but to those that secure, process, and control the materials upon which the future itself will be built.